As the cost of living crisis continues to bite, life in the capital is becoming increasingly unaffordable and young people are turning to social media ‘fin-fluencers’ for answers.

The perfect storm of high energy prices, rising interest rates and spiralling inflation is taking its toll across the UK, but London’s ranking as the fourth most expensive city in the world means Londoners’ pockets are particularly squeezed.

For many recent graduates moving to the big city, the prospect of making their salary stretch far enough seems daunting.

But instead of turning to traditional sources to learn more about money, young people are choosing to educate themselves elsewhere.

A new era of financial education

According to research by Lowell, one in five young Brits now rely on social media to seek financial advice.

Platforms such as TikTok and Instagram are home to a new generation of content creators known as ‘fin-fluencers’.

Instead of fashion or beauty tips they offer help with money management and investing, reaching thousands of young people with every post.

‘Fin-influencers’ based in the capital are becoming increasingly popular with young Londoners – the hashtag #londononabudget on TikTok has more than four million views alone, while #londoncheapeats has more than nine million hits.

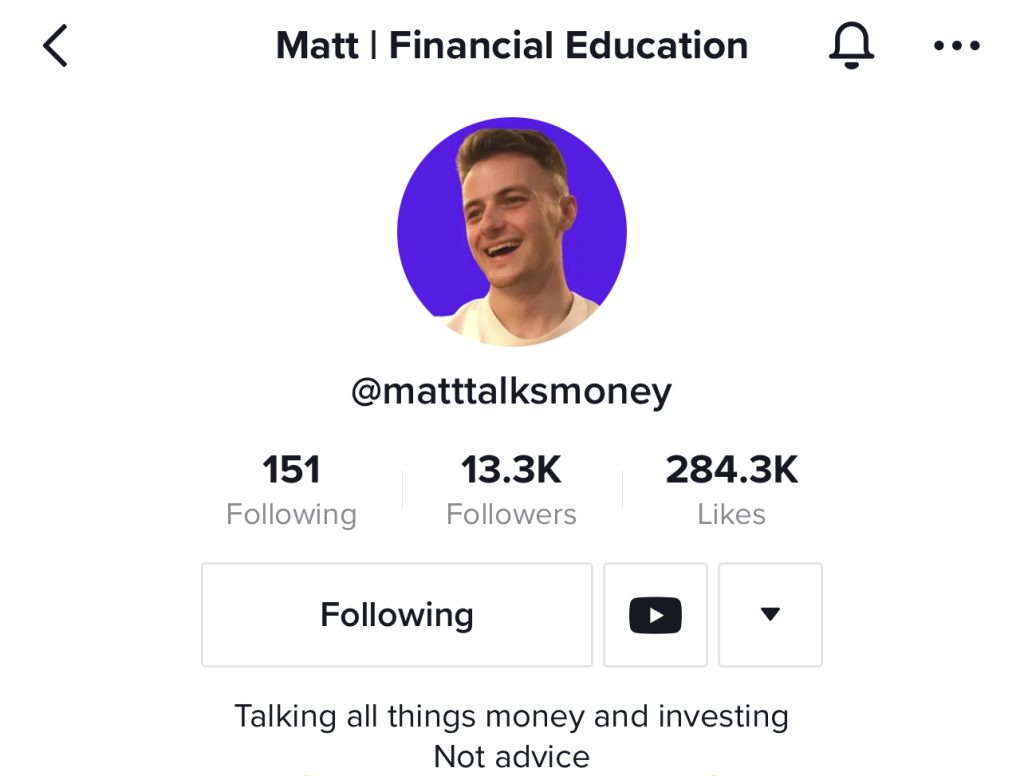

Matt Brady, a 22-year-old working in data marketing in London, has racked up more than 13,000 followers on TikTok providing financial education.

Since making his first post during lockdown in January 2021, he has expanded his content to Instagram and Twitter and created his own website.

His videos – filmed from his bedroom – are chatty and relaxed, explaining often-daunting financial jargon in a clear and engaging way.

He said: “The idea is to teach people about personal finance in a way that I would have loved to have been taught at school, or even at university.”

Amongst his most popular hits are videos showing how he budgets his graduate salary living in the capital.

“There were comments saying ‘you can’t survive on this in London,’ but I am, and I think it resonated with a lot of young people,” he added.

Matt also offers tips on various other financial topics, from investing for beginners to credit scores and how to improve them.

By posting freely accessible content, he hopes to reach and educate young Londoners who are struggling to make ends meet amid rising living costs.

“If you’re 21 and on a graduate salary and you’re already struggling financially, you’re not going to go and pay £500 for a money course,” he added.

Jessica Stewart Breen, a 21-year-old assistant manager from Dublin who recently moved to London, is one such graduate.

She said: “Moving from one capital to another capital, I was kind of aware of how expensive it would be, but I’m living in Central London so I don’t think anything could have ever prepared me for that.

“I feel like I’m living paycheck to paycheck no matter how hard I try to save.”

The rising cost of London life

Jessica is not alone – even a brief glance at recent statistics shows the financial odds are stacked against young people in London.

The average salary for a Londoner aged 22-29 is £30,092, according to the ONS.

Though this may seem generous in comparison to the equivalent nationwide figure of £24,600, the extra cash does little to cover the extremely high cost of living in the city.

The average rental value for new tenancies in London has soared by 11% in the last year to £1,945 a month, according to HomeLet.

The cost of day-to-day life is no cheaper either, with Numbeo estimating the average person spends £919.38 monthly excluding rent.

Moreover, for many recent graduates, their first job marks their first experience looking after their finances independently.

According to Lowell, 44% of young people say they are not confident managing their money, and 11% claim to have no confidence at all when it comes to personal finance.

Jessica found that social media and ‘fin-influencers’ offered concise and easy-to-understand content which helped to plug the gap left by a lack of education in school.

She said: “All that kind of information that isn’t necessarily available when you’re younger and if you haven’t figured it out at this age, it always feels like you’re starting at the bottom.

“When I tried to research online on normal websites like banks, the terminology they were using was just so not friendly to someone who’s a young person.

“I didn’t know what was going on.”

Bridging the gap

For Laura, founder of the popular Instagram page and blog Thrifty Londoner, demystifying the world of finance is a key part of her work.

The 30-year-old has amassed more than 17,500 followers on Instagram since first starting the account four years ago, and will soon leave her job as a senior brand manager to grow her ‘fin-fluencer’ brand full-time.

She said: “I started Thrifty Londoner to share money management tips, budgeting tips, investing, pensions – everything you can think of when it comes to money.

“Sometimes you have to use a little bit of jargon, but I think it really helps to explain what that jargon actually means.”

Laura believes social media helps foster a more personal connection between ‘fin-fluencers’ and their followers, breaking down the barrier preventing many young people from learning more about their finances.

She said: “I think it’s really the relatability factor – when people can see someone who is like them, they can relate to them and see a real face and a personal story behind things, which helps put things into context.

“It’s much less intimidating than going into a bank and being worried about not being taken seriously.”

According to the Young Money Report, 74% of young people aged 18-29 who follow ‘fin-fluencers’ trust the content they provide.

A word of warning

However, the sudden boom of ‘fin-fluencers’ has raised concerns about the danger of young people falling prey to misleading information online.

Users do not need financial qualifications to post money-related content on TikTok, meaning videos containing ill-informed advice can go viral and reach millions.

Susannah Streeter, 49, Senior Investment and Markets Analyst at Hargreaves Lansdown, warns against viewers trusting blindly in ‘fin-fluencers’ and financial information on social media as their money could be at risk.

She said: “In many ways, it’s really encouraging that social media is encouraging a more diverse range of investors to dip their tow in financial markets.

“But what is really concerning is that social media is where speculation really runs rife.”

She urges young people to be wary of influencers offering ‘personal’ advice or promoting a particular financial service, such as a high-risk investment or cryptocurrency.

Susannah added: “It’s great that people are getting involved in investing, but they have to make sure that they’re not getting swept up in the hype.

“It’s really important that you make your own judgements and seek independent advice elsewhere.”

Matt ensures he never offers personal financial advice to his followers, and has a disclaimer making this clear in the biography of his TikTok profile.

“Nobody on TikTok is a financial adviser unless they say they are so don’t take it as advice, take it as education and do your own research,” he said.

Laura takes the same approach but has struggled with fraudulent accounts which impersonate her and try to trick her followers into divulging personal financial information.

She said: “Certainly in the fin-fluencer community, lots of us are finding a similar issue and we are trying to campaign for something to be done about this.”

Time for tougher regulation?

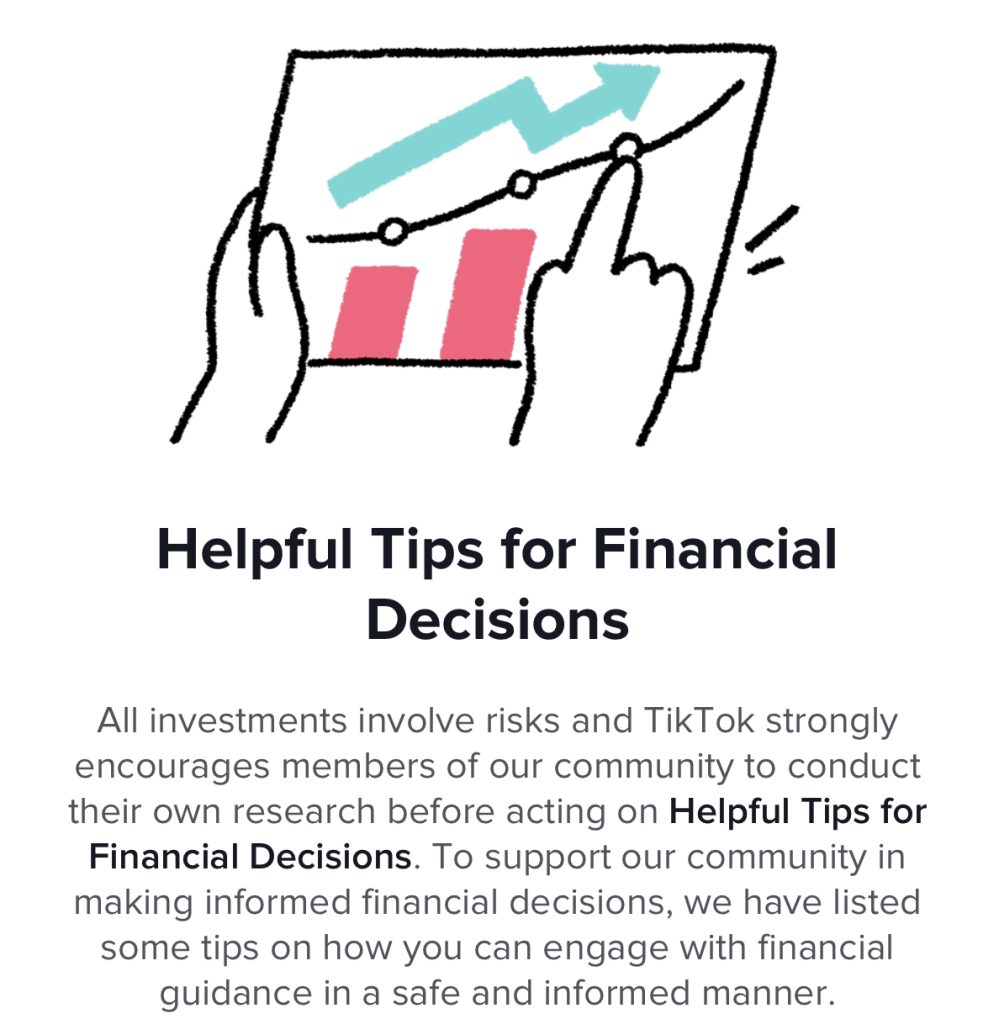

As the ‘fin-fluencer’ industry booms, calls are growing for tighter regulation of financial advice on social media.

Many TikToks discussing financial topics such as investing or credit cards are now flagged with a warning which directs users to a page entitled ‘Helpful Tips for Financial Decisions’.

In July 2021, the platform also updated its content policy to ban ‘fin-fluencers’ and other accounts from promoting specific financial services and products.

While such measures tackle the prevalence of fraudulent advice or promotion of high-risk investments, Susannah believes there is more to be done, particularly when it comes to paid promotions.

She said: “The rate of change that social media has brought into the financial services industry has been pretty breathtaking.

“Instagram and TikTok have got the money, and they’ve certainly got the know-how to create these algorithms to flag whether these are properly flagged as paid-for posts.”

Though further regulation appears likely, she adds that social media organisations can only do so much to protect their users.

Susannah added: “It is also up to individuals to take responsibility and think – why would I get financial advice from this person? Are they really the best person to be listening to? Should I at least verify what I’m saying with some other sites?”

You can find Laura on Instagram (@thriftylondoner) or on her website www.thriftylondoner.com.

You can find Matt on Tiktok (@matttalksmoney), Instagram (@matt.talksmoney) or on his website https://www.matttalksmoney.com/.